The Ticking Threat That Steals Your Dreams

Picture this: the joy of a new purchase with a credit card swipe, only for fear to creep in as the bill arrives. I’ve watched economies evolve since the 1960s, and today, America faces a debt time bomb. With $1.182 trillion in credit card debt and the sneaky rise of “Buy Now, Pay Later” (BNPL), your financial future hangs by a thread. Inflation bites at 2.73%, and unfair tariffs cost you $3,800 yearly. This isn’t just numbers—it’s your sleepless nights, your anger at a rigged system, and your hope to break free.

The Alarming Truth: A Nation Under Debt’s Weight

Credit Card Debt: An Explosive Rise

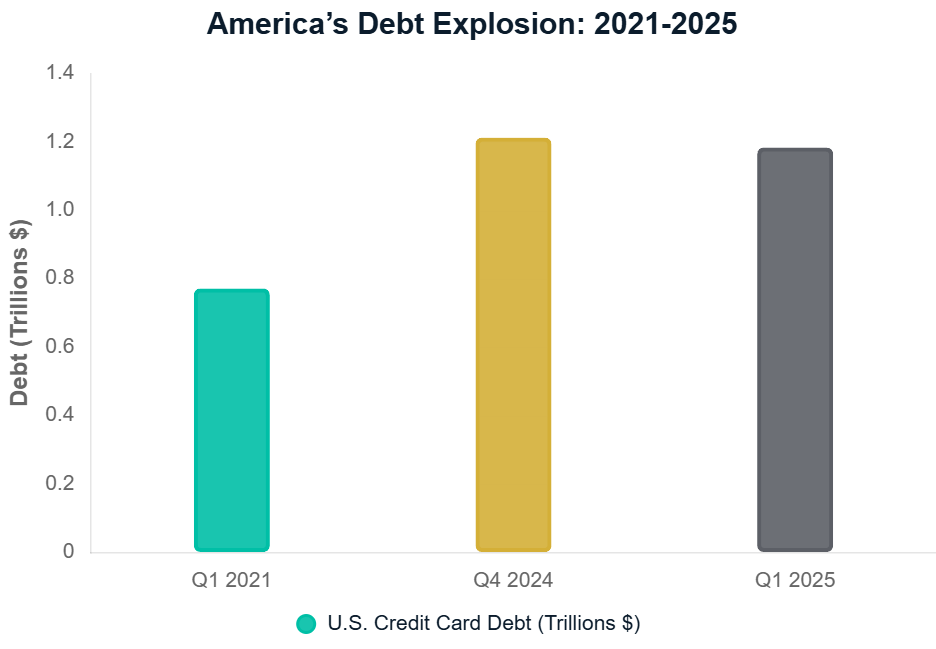

I remember the post-war boom when debt was a choice, not a necessity. Now, $1.182 trillion in credit card debt as of Q1 2025—down from $1.211 trillion in Q4 2024 but up 54% ($412 billion) since Q1 2021—weighs on families. It’s the panic of a missed payment, the joy of a rare clear month.

Table 1: Average Credit Card Debt by State (Q1 2025)

| State | Average Debt ($) | % Change (Q1 2024-2025) |

|---|---|---|

| New Jersey | 9,382 | +8.1% |

| Maryland | 9,252 | +8.4% |

| Connecticut | 9,201 | +2.4% |

| Massachusetts | 9,165 | +13.3% |

| California | 9,096 | +10.0% |

| Florida | 9,000 | +10.6% |

| Georgia | 7,943 | +20.5% (Fastest Growth) |

| Mississippi | 5,221 | – (Lowest) |

| Kentucky | 5,237 | – (Second Lowest) |

| Arkansas | 5,245 | – (Third Lowest) |

Source: Federal Reserve Bank of New York, Q1 2025

Georgia’s 20.5% jump fuels outrage at economic inequality, yet knowledge brings hope.

The APR Menace: A Costly Drain

APRs at 22.25% for existing cards and 24.35% for new offers in Q2 2025 feel like a slap—money lost to lenders’ greed.

The Silent Alarm: Delinquencies Signal Distress

Rising Delinquencies: A Warning Sign

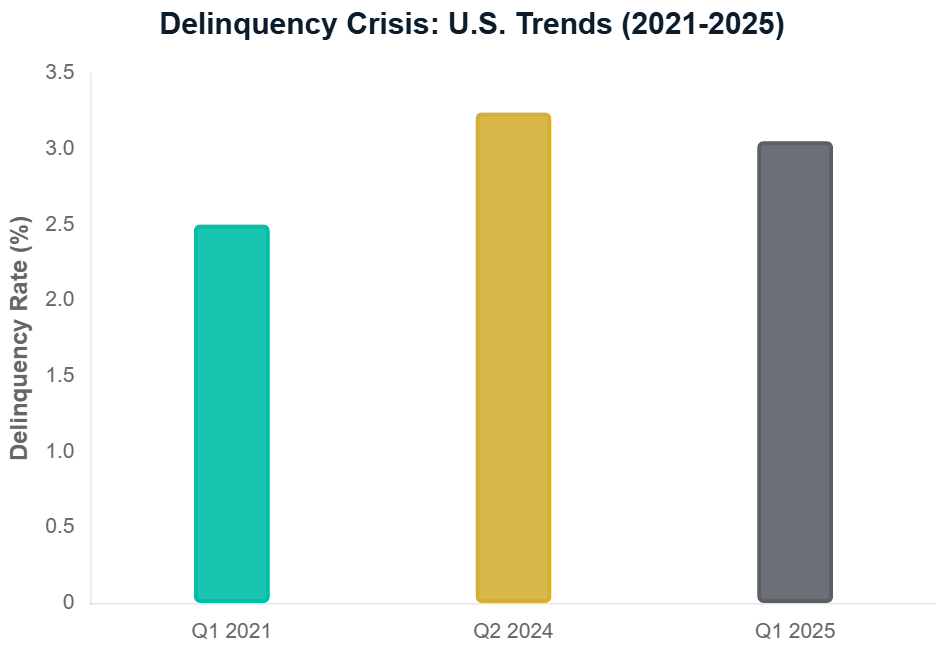

The delinquency rate (30+ days) eased to 3.05% in Q1 2025 from 3.24% in Q2 2024, but the climb since 2021 reflects hardship. Serious delinquencies linger, a stark reminder of struggle.

The Stealthy Invader: BNPL’s Hidden Peril

Usage Surge: A Desperate Turn

40% of Americans use BNPL, with 25% for groceries (up from 14% in 2024). It’s a heartbreaking necessity, fueling anger at exploitative systems.

FICO’s New Standard: A Critical Shift

From Fall 2025, FICO integrates BNPL data into credit scores, impacting payment history and utilization. Multiple loans mask risks—a wake-up call.

The Inflationary Squeeze: Pushing Credit Dependency

Rising Costs Squeeze Tight

Inflation at 2.73% in July 2025, 22.5% tariffs costing $3,800 per household, and 10% rent hikes since 2022 hit hard. The average salary ($66,622 in 2025) lags, sparking frustration and a search for stability.

The Deceptive Dance: How Debt Erodes Your Future

Minimum Payment Mirage

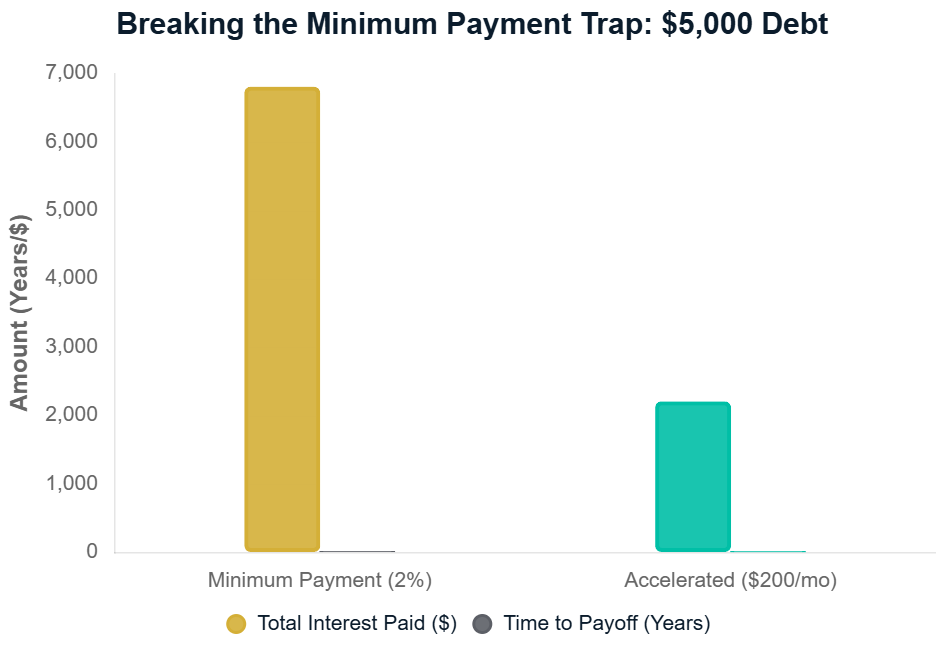

A $5,000 balance at 22% APR with a 2% minimum ($100) drags on for 10+ years, costing $6,800 in interest. Paying $200/month cuts it to 3 years and $2,200—a ray of hope.

| Scenario | Monthly Payment ($) | Total Interest ($) | Time to Payoff |

|---|---|---|---|

| Minimum Payment (2%) | 100 | 6,800 | 10+ Years |

| Accelerated | 200 | 2,200 | 3 Years |

Credit Utilization: A Downward Spiral

High utilization (above 30%) tanks credit scores, raising rates and rental hurdles—a cycle of despair you can shatter.

Your Escape Plan: Reclaim Financial Power

Step 1: Face the Numbers with a Budget

Only 47% of Americans plan, and 80% feel money stress. The 50/30/20 Rule—50% Needs, 30% Wants, 20% Savings/Debt—brings clarity. Track with a notebook or app.

Step 2: Attack Debt—Avalanche or Snowball

- Avalanche: Crush the highest APR first to save.

- Snowball: Clear smallest debts for quick wins.

Step 3: Build an Emergency Fund

59% can’t cover a $1,000 emergency. Start with $500, then 3-6 months’ expenses—your safety net.

Step 4: Leverage Tools Wisely

Explore 0% APR balance transfers (12-18 months) or consolidation loans, but tackle spending habits.

Step 5: Master Your Credit Score

Check reports at AnnualCreditReport.com. BNPL now affects payment history (35%) and utilization (30%).

Beyond the Trap: Cultivating Resilience

Financial Literacy: Your Shield

87% regret not learning money skills in school. Read, attend seminars—knowledge fuels freedom.

The Long Game: Retirement

Median savings ($87,000) leave 47% at risk. Save post-debt for a joyful future.

Take Control: Your Future Awaits

The system profits from your confusion, but you can fight back. Craft a budget, tackle debt, and build savings. Your financial freedom is within reach—seize it with pride.